What is internal audit funcion?

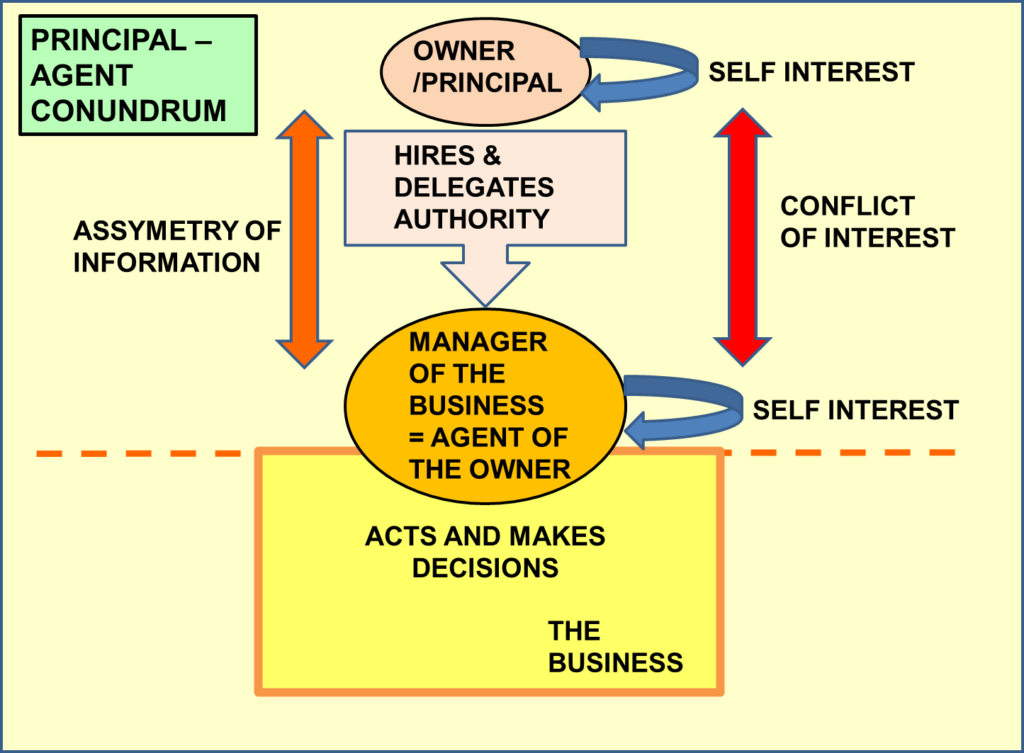

Managers are “agents” for the owners and are meant to serve the interests of the owners of the business as they manage the business. Placing managers in control of business activities creates an asymmetry of information between them and the owners of the business because managers have more information than owners. This asymmetry of information requires the owners to monitor managers effectively in order to ensure managers are indeed serving appropriately the interests of the owners of the business. Managers who are not also owners create “agency” risk and costs in case they do not not serve the owners’ interests as they discharge their duties as managers.

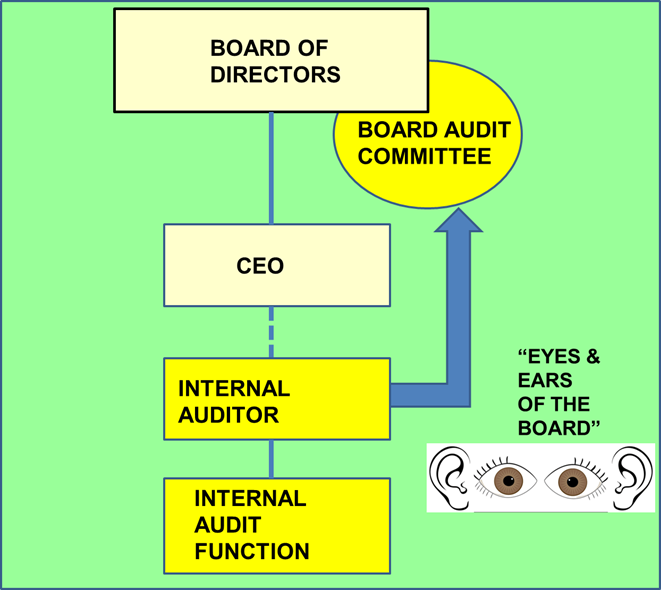

Internal monitoring of management becomes an important function that minimizes such agency risks and costs. This function is described as the “Internal Audit Function” and in order to preserve its independence from management and ensure its objectivity and effectiveness, it is common practice for the Internal Audit function not to report to the executive management but instead to report directly to the oversight body, very often the Board of Directors, which is elected by the owners or shareholders of the business and is tasked with keeping executive management accountable. The Internal Audit function is often likened to the “eyes and ears” of the Board of Directors.

Why does it matter ?

The Internal Audit function is one of the cornerstones of Corporate Governance. In its absence, management teams left without internal monitoring can take undue risks and cut corners in ways that undermine the prospects of the business. The Internal Audit function is meant to find and escalate critical issues to be heard at the Board. Historically, internal audit has been focusing on

- Financial impact of management actions/omissions

- Looking at past and current facts

- Delivering reports on finding on what went or may go wrong based on status quo

This function is evolving towards more holistic assessments across the business as a whole and including spotting future opportunities and challenges.

How do you introduce internal audit funcion?

Introducing an Internal Audit function is the responsibility of the oversight body of the business, most commonly the Board of Directors. The Board can mandate the creation of this function and the recruitment of the relevant personnel by the executive management. In turn, and in order to ensure its independence and thus enhance its effectiveness, the internal audit function is directly answerable to the Board.